Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024

It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024 Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowSemiconductor Industry Capital Spending to Grow 35% to $91B in 2017

November 16, 2017 | IC InsightsEstimated reading time: 2 minutes

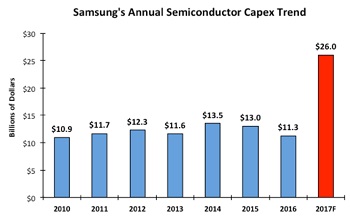

IC Insights’ latest forecast now shows semiconductor industry capital spending climbing 35% this year to $90.8 billion.

After spending $11.3 billion in semiconductor capex last year, Samsung announced that its 2017 outlays for the semiconductor group are expected to more than double to $26 billion. Bill McClean, president of IC Insights stated, “In my 37 years of tracking the semiconductor industry, I have never seen such an aggressive ramp of semiconductor capital expenditures. The sheer magnitude of Samsung’s spending this year is unprecedented in the history of the semiconductor industry.”

The figure shows Samsung’s capital spending outlays for its semiconductor group since 2010, the first year the company spent more than $10 billion in capex for the semiconductor segment. After spending $11.3 billion in 2016, the jump in capex expected for this year is simply amazing.

To illustrate how forceful its spending plans are, IC Insights anticipates that Samsung’s semiconductor capex of $8.6 billion in 4Q17 will represent 33% of the $26.2 billion in total semiconductor industry capital spending for this quarter. Meanwhile, the company is expected to account for about 16% of worldwide semiconductor sales in 4Q17.

IC Insights estimates that Samsung’s $26 billion in semiconductor outlays this year will be segmented as follows:

3D NAND flash: $14 billion (including an enormous ramp in capacity at its Pyeongtaek fab)

DRAM: $7 billion (for process migration and additional capacity to make up for capacity loss due to migration)

Foundry/Other: $5 billion (for ramping up 10nm process capacity)

IC Insights believes that Samsung’s massive spending outlays this year will have repercussions far into the future. One of the effects likely to occur is a period of overcapacity in the 3D NAND flash market. This overcapacity situation will not only be due to Samsung’s huge spending for 3D NAND flash, but also to its competitors in this market segment (e.g., SK Hynix, Micron, Toshiba, Intel, etc.) responding to the company’s spending surge. At some point, Samsung’s competitors will need to ramp up their capacity or loose market share.

Samsung’s current spending spree is also expected to just about kill any hopes that Chinese companies may have of becoming significant players in the 3D NAND flash or DRAM markets. As our clients have been aware of for some time, IC Insights has been extremely skeptical about the ability of new Chinese startups to compete with Samsung, SK Hynix, and Micron with regards to 3D NAND and DRAM technology. This year’s level of spending by Samsung just about guarantees that without some type of joint venture with a large existing memory suppler, new Chinese memory startups stand little chance of competing on the same level as today’s leading suppliers.

Details on capital spending and other trends within the IC industry are provided in The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry (released in January 2017). A subscription to The McClean Report includes free monthly updates from March through November (including the Mid-Year Update), and free access to subscriber-only webinars throughout the year. An individual-user license to the 2017 edition of The McClean Report is priced at $4,090 and includes an Internet access password. A multi-user worldwide corporate license is available for $7,090.

Share on:

Suggested Items

Digitalisation and ESG

04/19/2024 | Marina Hornasek-Metzl, AT&SDigitalisation and ESG are prominent and high-priority topics in the global business community. The first focuses on applying technology throughout the value chain to produce faster, smarter, and more desirable business outcomes. The latter emphasises the broader value a business is expected to create for its stakeholders from an environmental, social, and governance perspective.

Real Time with... IPC APEX EXPO 2024: Looking Back, Looking Forward With IEC

04/19/2024 | Real Time with...IPC APEX EXPOIEC came to the RTW booth and discussed both the legacy of IEC's past and the vision for its future. Industry veteran Bruno Ferri highlighted his quarter-century tenure in the industry and with IEC since its founding. He still exhibits boundless enthusiasm for the industry. Brando Stone, a young professional and a future face of IEC, talked about IEC's plans going forward and his experience at this year's IPC APEX EXPO.

Seeking Employment: Meet Parker Capers

04/18/2024 | Barry Matties, I-Connect007Parker Capers, a cybersecurity professional with a decade of experience in the SMT industry, earned a bachelor’s degree from DeVry and is CompTIA Security Plus certified. He is open to various industries but has a strong affinity for manufacturing due to extensive familiarity. Parker appreciates smaller companies where personal connections matter. Are you hiring?

SEMI Applauds CHIPS Program Office Progress to Diversify U.S. Semiconductor Industry Workforce

04/18/2024 | SEMIThe SEMI Foundation, the arm of SEMI dedicated to supporting economic opportunity for workers and the sustained growth of the microelectronics industry by creating pathways and opportunities for job seekers, applauded strides made by the CHIPS Program Office to diversify the U.S. semiconductor industry workforce and its release of the First Annual Report Regarding the Opportunities and Inclusion Activities Undertaken by the Department of Commerce.

VDMA: Machine Vision Navigating Through Uncertain Times

04/18/2024 | VDMAFor over a decade, the European machine vision industry has reported steady growth, with turnover increasing by an average of 9 percent annually between 2012 and 2022. Despite a temporary setback in 2020 (minus 4 percent) due to the Covid-19 pandemic, the industry rebounded strongly in 2021 (plus 17 percent) and 2022 (plus 11 percent).