Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024

It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024 Dan’s Biz Bookshelf: Seeing the How

Dan’s Biz Bookshelf: Seeing the HowCentral and Eastern Europe's Printing Market in Q4 2017: Inkjet Strikes Back

March 14, 2018 | IDCEstimated reading time: 3 minutes

The hardcopy peripherals (HCP) market in Central and Eastern Europe (CEE) grew 1.4% year on year in the fourth quarter of 2017, with shipments exceeding 1.7 million units, according to the Worldwide Quarterly Hardcopy Peripherals Tracker published by IDC. Shipment value in the same period increased 3.9% year on year to upwards of $493 million.

Inkjet shipments posted year-on-year growth of 12.6% in units and 14.3% in value. The inkjet market was characterized by a significant shift towards ink tank models. Ink tank models recorded 26.5% growth in unit terms. Ink tank printers represented more than 30% of the overall inkjet market in unit terms and over 48% in value in Q4 2017.

"Low cost per page and high ink yields make ink tank models attractive not only for consumers, but, increasingly, for business users, as well," says Ilona Stankeova, research director with IDC CEMA's Imaging, Hardware Devices, and Document Solutions group.

The laser market saw a decline of 5.7% in units compared to Q4 2016, but increased by 2.2% in value. While monochrome laser sales, especially those of cheaper entry-level models declined, color laser sales increased. Shipments of color laser MFPs increased 13.4% in units, supported by healthy growth of midrange and higher-end models, which are often delivered as part of a print service contract.

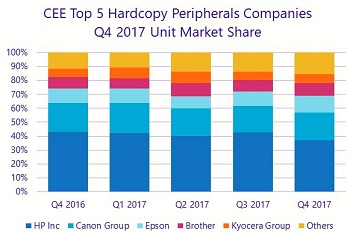

In terms of vendor ranking, HP Inc. remained the overall leader in the CEE hardcopy peripherals market in Q4 2017, with unit market share of almost 37% despite a shipment decline of 13.4% year on year. It is worth noting that Q4 2017 was the first quarter that HP Inc results included both HP- and Samsung-branded machines. While shipments of HP-branded machines recorded a moderate 7.8% decline, Samsung-branded shipments contracted by more than 40%.

Canon ranked second, with a minor decline in shipments and 19.9% market unit share. Epson's shipments increased by almost 17%, raising its market share to 12.0%. Although Brother ranked fourth, it outperformed the market with shipment unit growth of 18.4%.

Country Highlights

Russia

The Russian HCP market recorded a 6.0% increase in units and a 9.1% increase in value year on year in Q4 2017. Although still below pre-crisis levels, the Russian market, started to show signs of recovery in 2017. The gradual improvement of the economy, as well as GDP growth resulting from stabilization of the ruble and an increase in crude oil prices helped boost the Russian market. Both inkjet and laser market segments recorded positive unit growth, of 3.5% and 7.6%, respectively. Ink tank models represented close to 39% of the inkjet market in units and more than 57% of the overall value.

Poland

After several quarters of decline, the Polish market posted growth of 10.5% in units and 2.6% in value in Q4 2017. Inkjet shipments recorded remarkable unit growth of 28.0%, supported by both consumer and business demand, while laser unit shipments declined over 9%. Ink tank models represented 15.4% of the inkjet market in unit terms and more than 28% in value.

The positive result in Q4 did not balance the previous quarters of decline, however. The total Polish HCP market recorded an annual decline in units of 3.2% and of 7.4% in value in 2017 when compared to 2016 annual results.

Czech Republic

Contrary to Poland, the Czech HCP market declined in Q4 2017, after several quarters of moderate growth. The dynamics for ink and laser segments were similar to that seen in Poland: while the Czech inkjet market recorded a 3.6% increase in units, the laser market declined almost 13%. Shipments of ink tank models experienced double-digit growth, and ink tank sales represented 17.0% of the total inkjet market in units and close to 30% in value.

About IDC

International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,100 analysts worldwide, IDC offers global, regional, and local expertise on technology and industry opportunities and trends in over 110 countries. IDC's analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives. Founded in 1964, IDC is a wholly-owned subsidiary of IDG, the world's leading media, data and marketing services company that activates and engages the most influential technology buyers. To learn more about IDC, please click here.

Share on:

Suggested Items

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.

Real Time with... IPC APEX EXPO 2024: Exploring Silicone Solutions with R&D Director of CHT

04/17/2024 | Real Time with...IPC APEX EXPOIn this interview, Gerry Ellis, the R&D director for CHT, discusses the product range offered by his company. He explains the challenges in creating base formulations, the drive to make products more user-friendly, and the various application techniques involved. Ellis also highlights the key market segments and the significance of providing efficient solutions to customers.

Gartner Forecasts Worldwide IT Spending to Grow 8% in 2024

04/17/2024 | Gartner, Inc.Worldwide IT spending is expected to total $5.06 trillion in 2024, an increase of 8% from 2023, according to the latest forecast by Gartner, Inc. This is an increase from the previous quarter’s forecast of 6.8% growth and puts worldwide IT spending on track to surpass $8 trillion well before the end of the decade.