Marcy's Musings: The Growing Industry

Marcy's Musings: The Growing Industry It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024

It’s Only Common Sense: Here’s What To Do After IPC APEX EXPO 2024 Dan’s Biz Bookshelf: Seeing the How

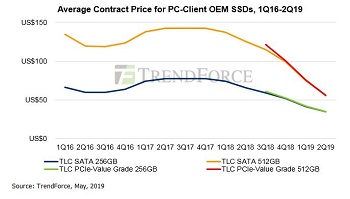

Dan’s Biz Bookshelf: Seeing the How512GB SSDs' Price-per-GB Estimated to Hit an All-time Low This Year End

May 8, 2019 | TrendForceEstimated reading time: 2 minutes

According to research by DRAMeXchange , a division of TrendForce , the NAND flash industry this year is clearly exhibiting signs of oversupply, and SSD suppliers have gotten themselves into a price war, causing SSD prices for PC OEMs to take a dive. Average contract prices for 512GB and 1TB SSDs have a chance to plunge below US$0.1 per GB by the end of this year, hitting an all-time low. This change will cause 512GB SSDs to replace their 128GB counterparts and become market mainstream, second only to 256GB SSDs. We may also look forward to PCIe SSDs achieving 50% market penetration, since PCIe SSDs and SATA SSDS are nearly identical in price.

TrendForce points out that SSD adoption among notebooks had already come above the 50% threshold in 2018. Contract prices for mainstream 128/256/512GB SSDs have fallen a long way by over 50% since peaking in 2017, and those for 512GB and 1TB SSDs have a chance to fall below US$0.1 per GB by year-end. This will stimulate demand from those seeking to replace their 500GB and 1TB HDDs. SSD adoption rate is expected to land between 60 and 65% in 2019.

2Q Average Contract Prices for SSDs to Fall by Double Digits, May Drop by Less in 3Q

According to TrendForce's latest investigations, 2Q19 marks the 6 th consecutive quarter of average contract price decline for mainstream PC-Client OEM SSDs, with the average contract price for SATA SSDs falling QoQ by 15-26%, and PCIe SSDs by 16-37% .

The reasons for the continuous price fall in 2Q include: weakened stocking momentum due to the cautious stance of PC, smartphones, servers/datacenters OEMs towards end market sales and high inventory levels, leading to an overly oversupplied NAND flash market; prices wars by leading SSD suppliers who are keen to get their 64/72-layer stocks off their hands; and the price comparison effect as a result of Intel 3D QLC SSDs.

The demand side will be helped by the traditional peak season and increased stocking demand from the new Apple devices, possibly seeing an improvement over 1H in 3Q looking forward. Furthermore, many NAND flash suppliers are slowing expansion plans and have declared reductions in production to curtail supply. Yet judging from the rather high inventories along this chain of industry, TrendForce predicts that average contract prices for mainstream SSD capacities will likely continue their descent, although with a slope less steep.

Price Differences Greatly Narrow, with PCIe to Replace SATA Interfaces as Market Mainstream

Judging from the product progress of each SSD supplier, all mainstream product lines have already switched to 64/72 layer SSDs with 256/512GB capacities and PCIe interfaces as their main products. The newest 96-layer SSD has also gradually entered production in 1Q this year. Additionally, judging from average contract prices in the second quarter, current prices for Premium PCIe SSDs and SATA SSDs only differ by under 6%, while value grade PCIe SSDs and SATA SSDs register a nearly 0% difference. PCIe interfaces, with the help of value grade PCIe SSDs, will replace SATA interfaces to become market mainstream this year.

About TrendForce

TrendForce is a global provider of the latest development, insight, and analysis of the technology industry. Having served businesses for over a decade, the company has built up a strong membership base of 435,000 subscribers. TrendForce has established a reputation as an organization that offers insightful and accurate analysis of the technology industry through five major research divisions: DRAMeXchange, WitsView, LEDinside, EnergyTrend and Topology. Founded in Taipei, Taiwan in 2000, TrendForce has extended its presence in China since 2004 with offices in Shenzhen and Beijing.

Share on:

Suggested Items

IDTechEx Examines the Opportunities for Wearables in Digital Health

04/19/2024 | IDTechExIDTechEx’s report, “Digital Health and Artificial Intelligence 2024-2034: Trends, Opportunities, and Outlook”, covers this ongoing trend in the consumer health wearables market and includes analysis of the opportunities and roadmap for biometric monitoring.

Real Time with... IPC APEX EXPO 2024: Pluritec's Expansion and Growth in the North American Market

04/19/2024 | Real Time with...IPC APEX EXPONicola Doria, president of Pluritec, discusses the company's strategic focus on the North American market, their investment in a new sales organization, service expansion, and a new process integration line. The conversation also covers market response and future installations, as well as Pluritec's new partnership with IEC.

Mycronic Releases Interim Report January–March 2024

04/18/2024 | MycronicNet sales increased 39 percent to SEK 1,692 (1,219) million. Based on constant exchange rates, net sales increased 42 percent.

Real Time with... IPC APEX EXPO 2024: Exploring Silicone Solutions with R&D Director of CHT

04/17/2024 | Real Time with...IPC APEX EXPOIn this interview, Gerry Ellis, the R&D director for CHT, discusses the product range offered by his company. He explains the challenges in creating base formulations, the drive to make products more user-friendly, and the various application techniques involved. Ellis also highlights the key market segments and the significance of providing efficient solutions to customers.

Gartner Forecasts Worldwide IT Spending to Grow 8% in 2024

04/17/2024 | Gartner, Inc.Worldwide IT spending is expected to total $5.06 trillion in 2024, an increase of 8% from 2023, according to the latest forecast by Gartner, Inc. This is an increase from the previous quarter’s forecast of 6.8% growth and puts worldwide IT spending on track to surpass $8 trillion well before the end of the decade.